My learning journey in Derivatives Markets

My learning journey in Derivatives Markets has been an exciting and challenging one. As someone with a background in finance, I have always been interested in learning more about derivatives markets and the various strategies used to mitigate risks and maximize returns.

The course began with an overview of derivatives markets and the different types of instruments traded in these markets. We then delved deeper into the mechanics of options, futures, and swaps, and learned how these instruments can be used to hedge risks and speculate on market movements.

One of the most challenging aspects of the course was learning about the advanced mathematical models used to price derivatives. We spent several weeks studying Black-Scholes and other models, and I was amazed by the level of complexity involved in these calculations. However, with the help of my instructor and classmates, I was able to grasp these concepts and gain a deeper understanding of the pricing mechanisms underlying derivatives markets.

Another aspect of the course that I found particularly interesting was learning about the various trading strategies used by market participants. We studied everything from simple long and short positions to more complex strategies such as straddles and spreads. We also learned about the importance of risk management and how to construct portfolios that minimize risk while maximizing returns.

Throughout the course, we worked on several case studies and group projects that allowed us to apply the concepts we had learned to real-world scenarios. These projects were challenging but rewarding, as they helped us to develop our analytical skills and gain practical experience in derivatives trading.

Week 1: Forward Contracts

In our first week, we focused on Forward Contracts and learned about the following key points:

- We started by understanding what Forward Contracts are and how they differ from other types of financial instruments such as options and futures.

- We then delved into the key features of Forward Contracts, such as their fixed price, delivery date, and customized nature.

- Finally, we explored real-world examples of how Forward Contracts are used in different industries, such as agriculture and energy, and how they can be combined with other financial instruments to create more complex trading strategies.

I found some problems quite interesting:

Part 3

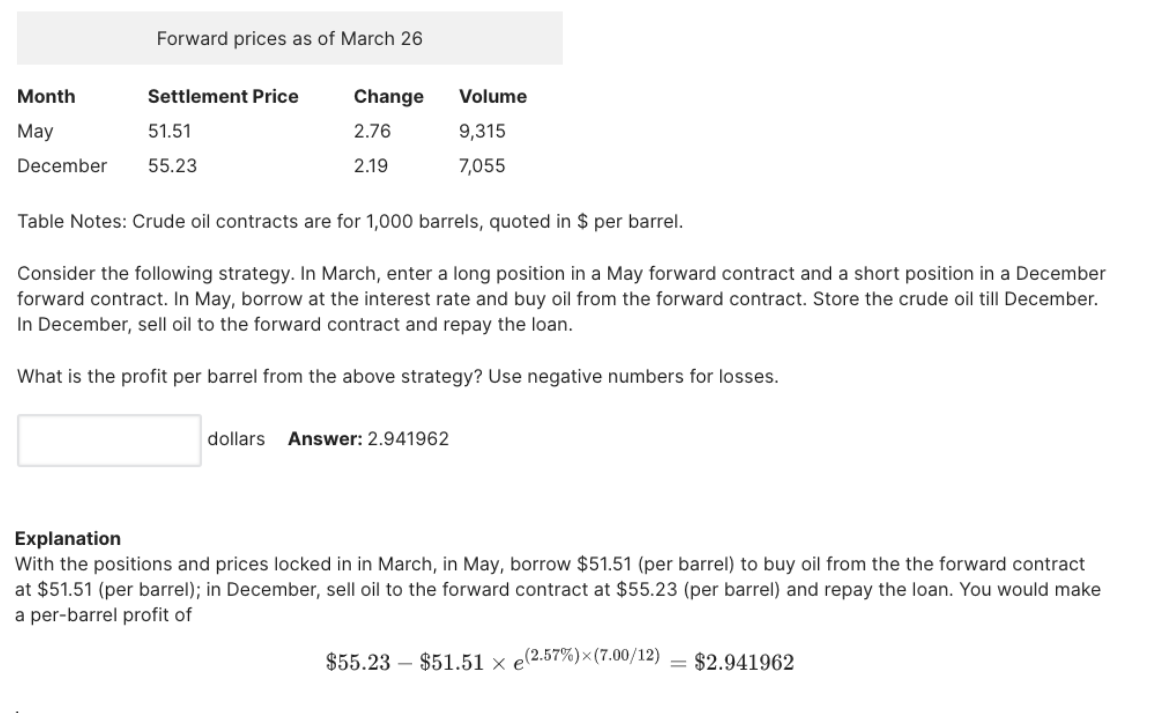

Suppose that there are no storage costs for borrowing or lending is 2.57% per annum(continuously compounded). Consider the transactions that would allow you to make an arbitrage profit in March by trading in May and December forward contracts. Use the forward prices provided in the table below and assume you can lock in the settlement prices on either a long or short position.

Week 2: Futures and Swaps

As a student of Derivatives Markets, I found our second week of studying Futures and Swaps to be incredibly insightful. Here are three key points that stood out to me:

- We started by learning about what Futures and Swaps are and how they differ from each other and other types of financial instruments. Futures contracts involve standardized terms and are traded on exchanges, while Swaps are customized agreements between two parties and are traded over-the-counter.

- We then discussed the key features of Futures and Swaps, such as their fixed price, delivery date, and underlying asset.

- Finally, we explored the risks and benefits associated with Futures and Swaps, including counterparty risk, margin requirements, and liquidity.

I found some problems quite interesting:

Part 4

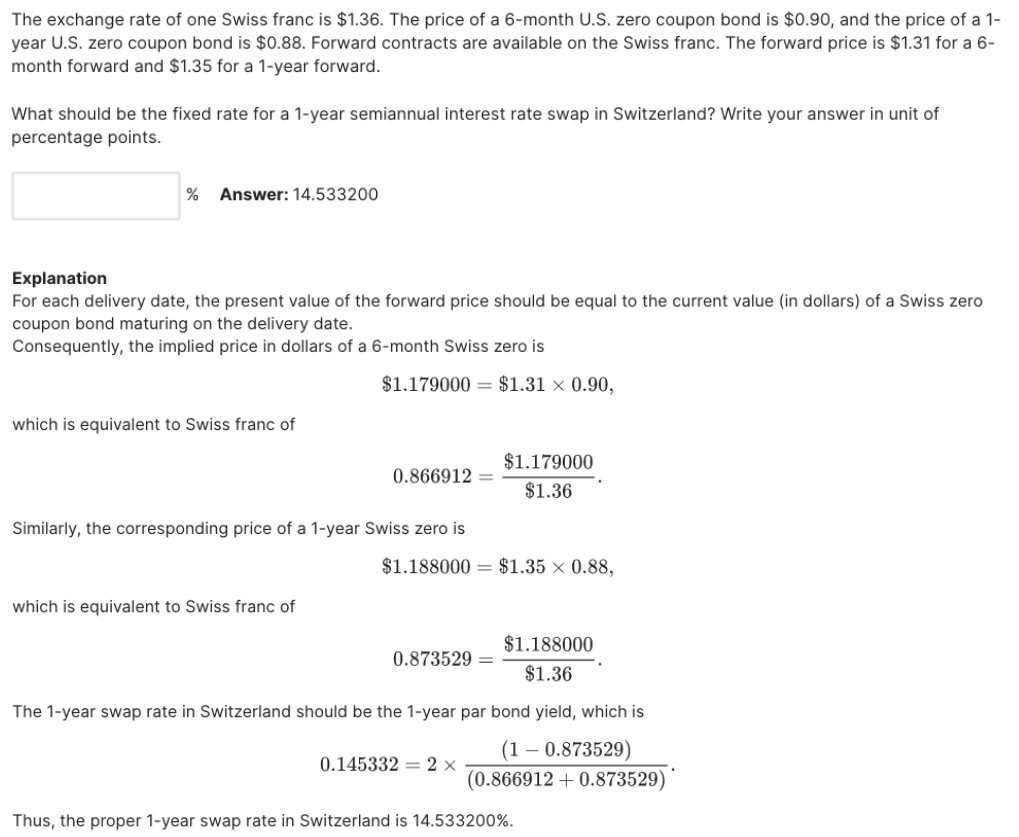

Find the fixed rate for a 1-year semi annual interest rate swap for the following.

Week 3: Duration-based Strategies

I found our third week of studying Duration-based Strategies to be incredibly interesting. Here are three key points that stood out to me:

Definition and Importance: We started by learning about what Duration is and how it measures the sensitivity of a bond’s price to changes in interest rates.

Strategies: We then explored different Duration-based strategies, such as matching the Duration of assets and liabilities, barbell and bullet strategies, and immunization strategies.

Real-world Examples: Finally, we looked at real-world examples of Duration-based strategies used by institutional investors, such as pension funds and insurance companies. We also discussed how changes in interest rates and economic conditions can affect the performance of these strategies.

I found some problems quite interesting:

Part A

Assume that the treasury yield curve is flat at 3% on an annual basis (i.e., an investment of $100 receives a 3% interest payment at the end of the year).

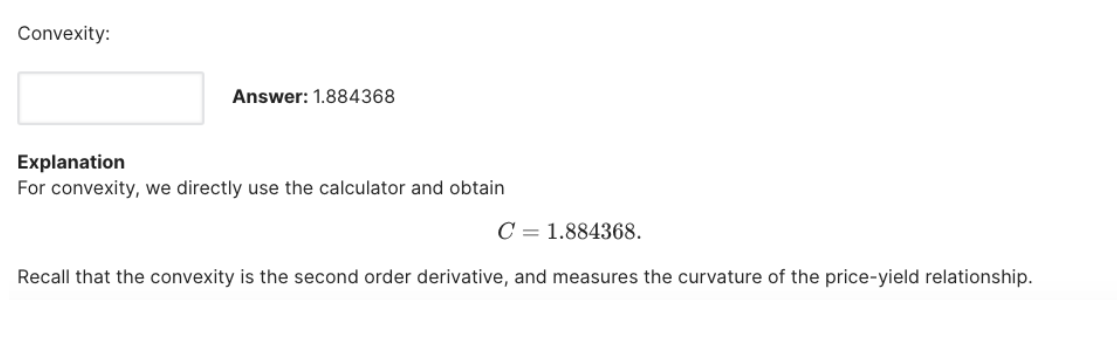

Utilize the duration and convexity calculator and answer the following.

Overall, my learning journey in Derivatives Markets: Advanced Modeling and Strategies was a challenging but incredibly rewarding experience. I gained a deep understanding of the mechanics of derivatives markets and the various strategies used to trade in these markets. I also developed my analytical skills and gained practical experience through case studies and group projects. I am excited to continue exploring this fascinating field and applying what I have learned to my future endeavors in finance.

To view the full journey, please visit: